A financial crisis is more than just a bad day on Wall Street; it is a systemic breakdown where the very gears of the global economy grind to a halt. When a crisis hits, asset prices plummet, businesses face insolvency, and financial institutions struggle with severe liquidity shortages. It often triggers a “domino effect,” where fear leads to bank runs and irrational sell-offs, turning a localized problem into a global recession.

1. The Anatomy of a Crisis: Why Do Systems Fail?

Financial crises rarely have a single source. Instead, they are the result of a “perfect storm” of economic and behavioral factors.

Asset Overvaluation & Bubbles: When investors drive prices far beyond their intrinsic value (speculation), a “bubble” forms. When it inevitably bursts, the resulting capital loss wipes out trillions in wealth.

Systemic Regulatory Failure: A lack of oversight often encourages financial institutions to take on excessive leverage. Without “guardrails,” the system becomes fragile.

The Contagion Effect: In our interconnected world, a currency crisis in one nation can act like a virus, spreading to trading partners and triggering a regional or global meltdown.

Human Behavior: Panic is a powerful economic force. Herd-like behavior—where everyone tries to exit a market simultaneously—destroys market liquidity, making it impossible for even healthy firms to find case

2. Historical Benchmarks: From Tulips to Toxic Debt

To understand the present, we must look at the “scar tissue” of economic history.

2.1 The Great Crash of 1929

Triggered by wild speculation and an oversupply of commodities, this crash led to the Great Depression. It remains the benchmark for economic suffering, lasting over a decade and fundamentally changing global financial regulation.

2.2 The 1973 OPEC Oil Crisis

This was a rare “supply-side” crisis. An oil embargo sent prices skyrocketing, leading to stagflation—a painful mix of stagnant economic growth and high inflation. The Dow Jones lost 43% of its value as the world realized its dangerous dependence on a single energy source.

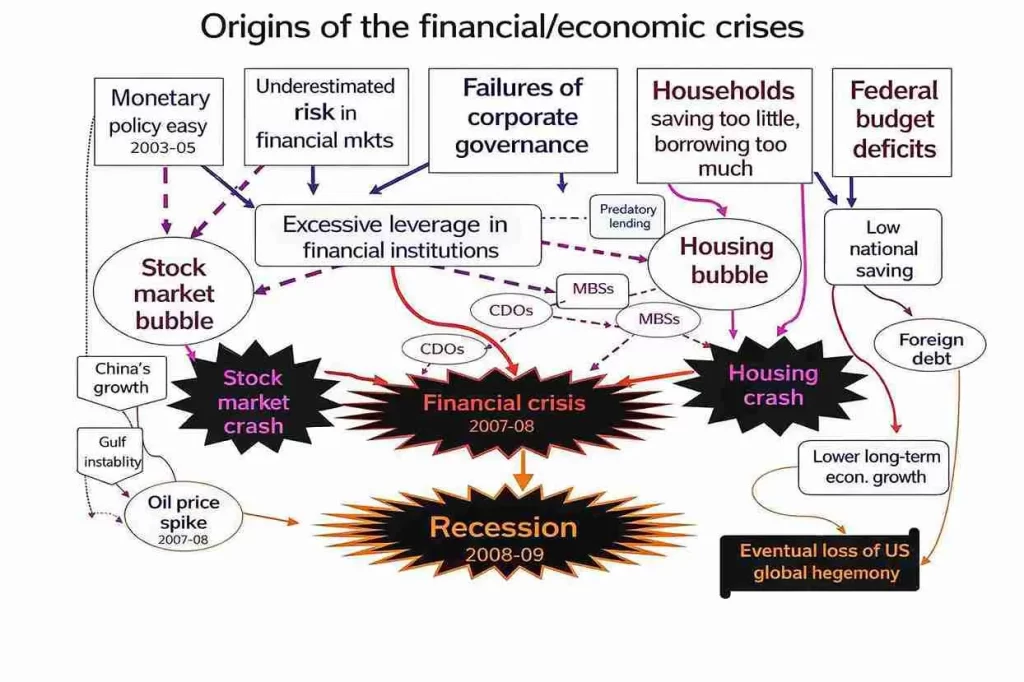

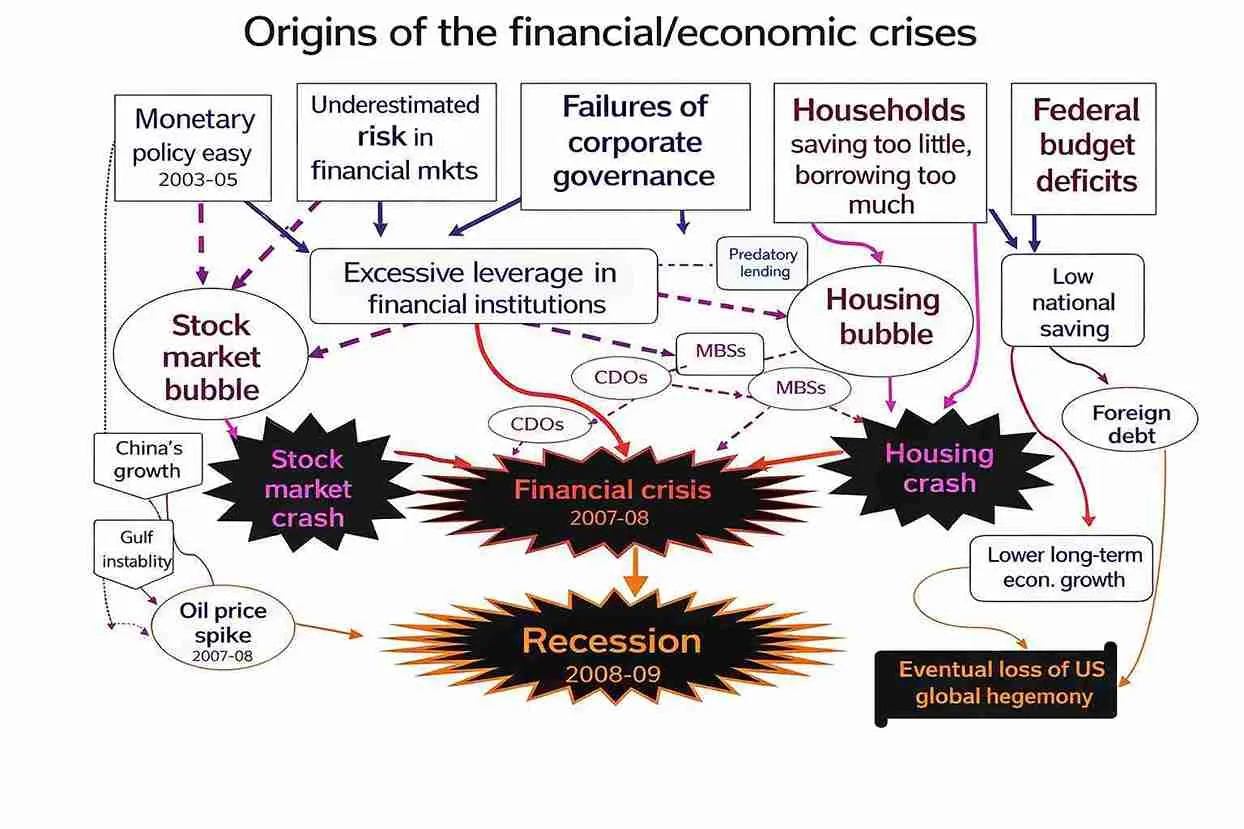

2.3 The 2008 Global Financial Crisis (GFC)

The GFC was the most significant disaster since 1929. It began with subprime mortgage lending—loans given to high-risk borrowers. These “toxic” debts were bundled into complex Collateralized Debt Obligations (CDOs) and sold to unsuspecting investors.

The Trigger: When the housing bubble burst, defaults spiked.

The Collapse: Icons of finance like Lehman Brothers vanished overnight.

The Fallout: The U.S. government stepped in with a massive taxpayer-funded bailout to prevent total systemic collapse. This led to the Dodd-Frank Act, which introduced stricter capital requirements and oversight for the banking sector.

3. The 2020 COVID-19 Shock: A Different Breed of Crisis

Unlike 2008, the 2020 crisis wasn’t caused by “bad math” in the banking system, but by a biological external shock.

The Impact: Global supply chains froze, and the S&P 500 lost 34% of its value in just one month.

The Response: Central banks slashed interest rates to near zero and launched massive monetary stimulus packages.

The Recovery: Remarkably, the markets rebounded quickly, hitting new highs by 2021. However, the long-term macroeconomic consequences—including high inflation and increased sovereign debt—are still being felt today in 2026.

4. Key Takeaways for the Modern Investor

Understanding the lifecycle of a crisis is essential for risk mitigation. While every crisis feels unique, they all share common themes: over-borrowing, regulatory absence, and irrational exuberance.

| Type of Crisis | Primary Trigger | Example |

| Banking Crisis | Liquidity shortage / Bank runs | 1930s Great Depression |

| Speculative Bubble | Irrational overvaluation | 1637 Tulip Mania |

| Sovereign Default | Government inability to pay debt | 2010s Greek Debt Crisis |

| External Shock | Non-economic disasters | 2020 COVID-19 Pandemic |

The Bottom Line

A financial crisis is an inherent feature of the modern business cycle. While we cannot always predict the next “black swan” event, we can understand the mechanics of leverage and liquidity to better protect our assets. The goal isn’t just to survive the crash, but to understand the market dynamics well enough to recognize the recovery on the horizon.