In the realm of global finance, tax and revenue collection serves as the lifeblood of a functioning state. It is the primary mechanism for funding public services, infrastructure, and redistribution. However, this sector remains one of the most vulnerable to fiscal corruption. When the integrity of a tax system is compromised, it doesn’t just result in a ledger deficit; it triggers a systemic breakdown of the social contract between the government and its citizens.

1. The Mechanics of Tax-Related Corruption

Corruption in revenue collection arises from a complex interplay of administrative loopholes, political incentives, and private interests. At its core, it is a game of collusion where both the collector and the taxpayer find a mutually beneficial, albeit illegal, arrangement.

1.1 Administrative Discretion and Bureaucratic Pressures

The primary driver for corruption within tax administrations is the vast discretionary power granted to officials. When tax laws are overly complex and lack transparency, officials can create artificial “red tape” to solicit bribes. Conversely, taxpayers—particularly high-net-worth individuals and corporations—may offer kickbacks to secure tax exemptions or “dubious loopholes.” This regulatory capture ensures that the wealthy can bypass their legal obligations, leaving the fiscal burden to fall disproportionately on the compliant middle class.

1.2 The Political Weaponization of Revenue

Beyond personal greed, revenue collection is often politicized to serve the interests of the ruling elite.

Patronage and Clientelism: Governments may grant preferential customs rates or tax breaks to political allies and “crony” corporations to maintain power.

Suppression of Dissent: In illiberal regimes, the tax code is frequently weaponized. Harsh audits and trumped-up charges of tax evasion are used as tools for political repression against opposition figures, journalists, and NGOs.

Slush Funds: Embezzled tax revenues are often siphoned into “off-budget” accounts to finance election campaigns or maintain the loyalty of the military and security apparatus.

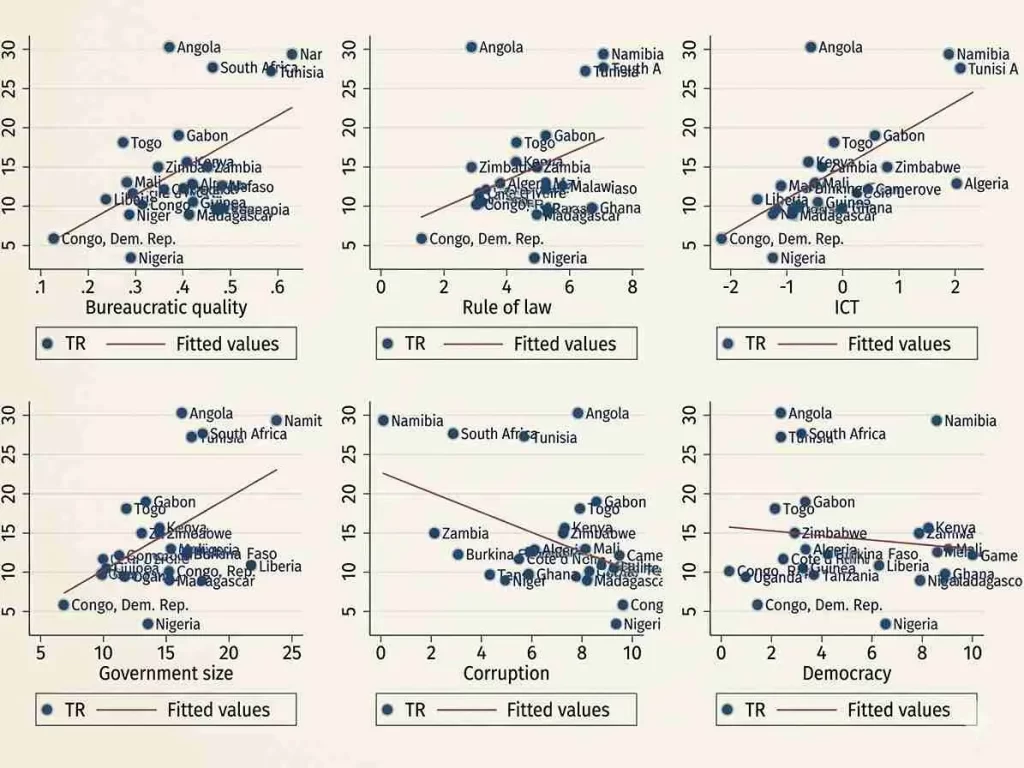

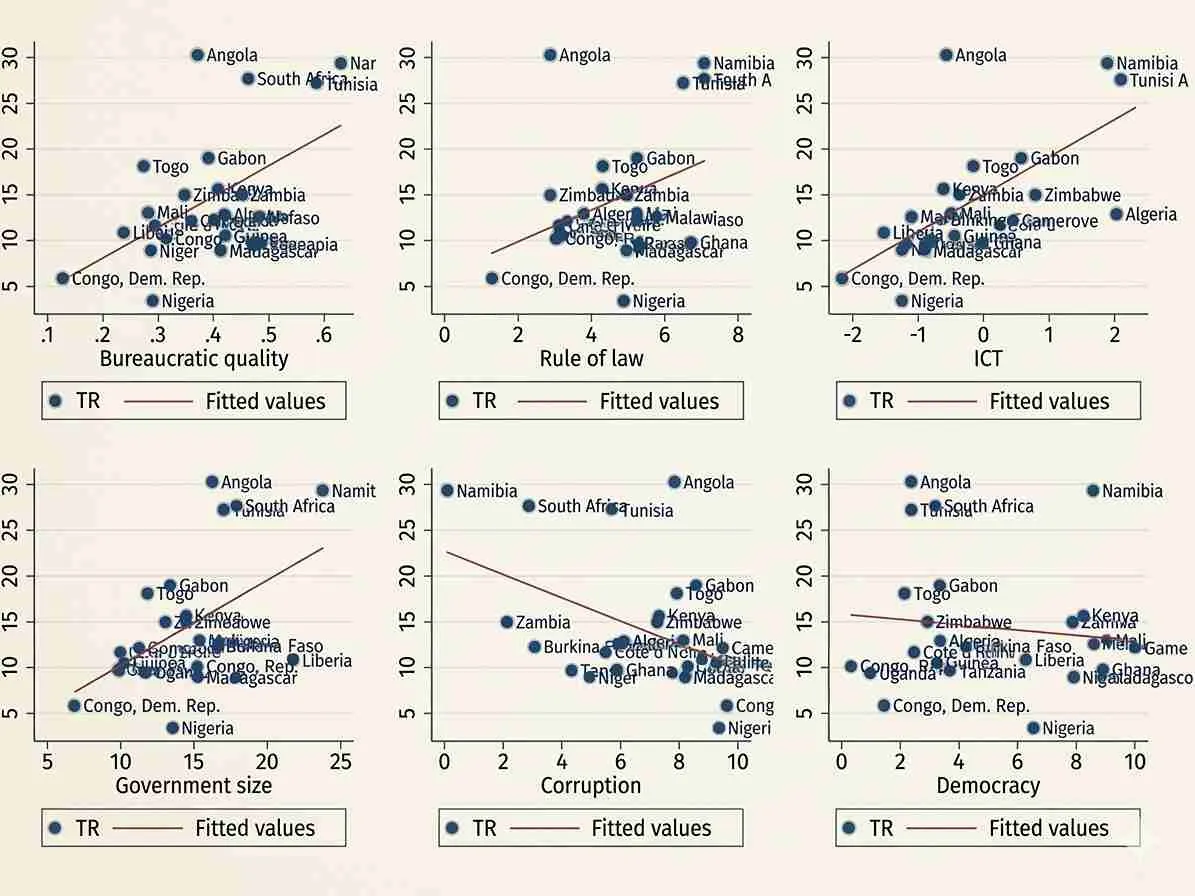

(Note: While the image above depicts a general crisis, fiscal corruption often acts as the primary catalyst for the “Systemic Failure” stage.)

2. The Macroeconomic Fallout: Illicit Financial Flows (IFFs)

The consequences of fiscal corruption extend far beyond national borders. The capital siphoned off through bribery and commercial tax fraud constitutes a major portion of Illicit Financial Flows (IFFs). These funds are typically moved through shell companies and hidden in offshore tax havens, facilitated by a network of professional enablers—lawyers, accountants, and financial consultants.

This drainage of capital is particularly devastating for developing nations. It creates a “downward spiral”: as public trust in government legitimacy fades, tax morale collapses. If citizens perceive their leaders as corrupt, they no longer feel a moral obligation to comply with tax laws, further depleting the treasury and crippling public service delivery.

3. Rentier States vs. Fiscal States

A fascinating dimension of this issue is the “Resource Curse.” Rentier states—those that derive the majority of their revenue from natural resources (like oil or minerals)—often have the weakest tax systems. Because the government does not rely on a tax-paying citizenry for its survival, the social contract is effectively severed. The leadership becomes accountable only to the few corporations extracting the resources, leading to high levels of embezzlement and a total lack of transparency.

4. Strategic Approaches to Reform

Technical reforms alone are rarely enough to curb corruption if the political will is absent. However, where a genuine desire for reform exists, several high-impact strategies can be deployed:

Semi-Autonomous Revenue Authorities (SARAs): Granting tax agencies independence from direct political interference can reduce the pressure to grant “favors.”

Digitalization and Automation: Investing in e-government solutions reduces face-to-face interaction between taxpayers and collectors, closing the window for bribery.

Whistleblower Protections: Encouraging the reporting of corruption through secure channels and financial incentives.

Strengthening Executive Constraints: Robust checks and balances and independent audits are essential to ensure the impartial application of the tax code.

The Bottom Line

Corruption in tax collection is a fundamental barrier to sustainable economic development. It undermines the rule of law and reinforces illiberal regimes. In 2026, as global markets face increasing volatility, the transparency of a nation’s fiscal system will be a key determinant of its sovereign credit rating and its ability to attract legitimate foreign investment.