Financial wellbeing is not merely a destination; it is a state of being secure and in control of your daily finances. In an era of economic shifts, effective Personal Financial Management is the differentiator between those who simply earn and those who truly thrive. At its core, this discipline is about having the confidence that you can manage the unexpected while steadily building a prosperous future.

To achieve true financial independence, you must move beyond basic saving and adopt a strategic Personal Financial Management framework. This starts with the most fundamental tool in your arsenal: The Budget.

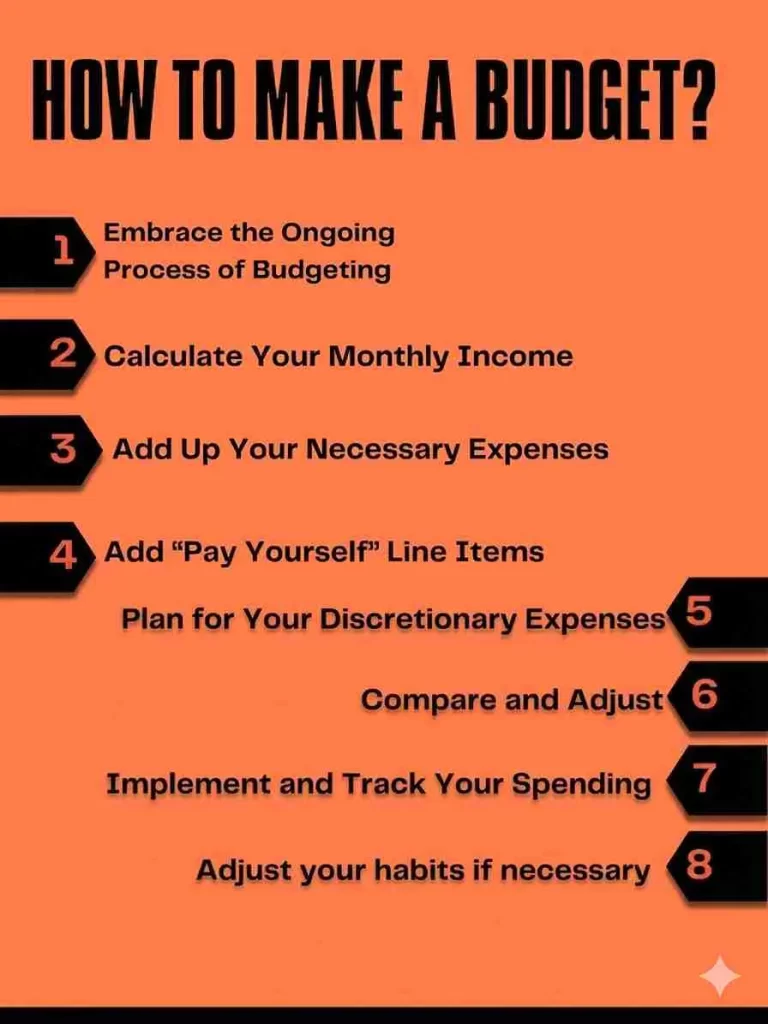

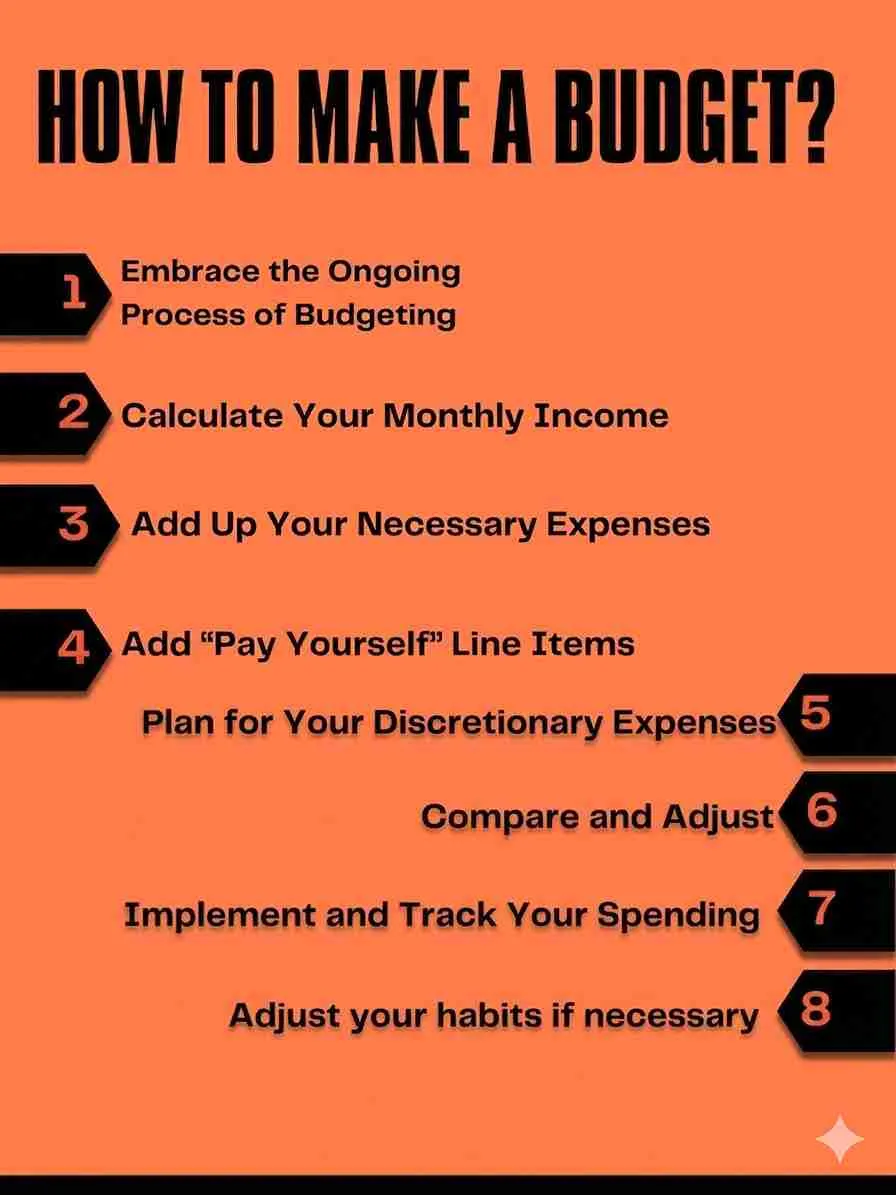

1. The Foundation: Income, Expenditure, and Strategic Budgeting

A budget is not a restriction; it is a Spending Plan designed to give you greater peace of mind. The first step in professional Personal Financial Management is to conduct a rigorous audit of your Cash Flow.

Audit Your Income: Average your regular earnings over the last three months to establish a baseline.

Track Your Outgoings: Use digital tools like the HSBC Vietnam App to monitor every transaction. True mastery of Personal Financial Management requires accounting for both digital payments and those “hidden” cash purchases that often go unrecorded.

By comparing these two figures, you can instantly see if you are living beyond your means or if you have a surplus to fuel your Investment Strategy.

2. Setting Milestones: The Goal-Oriented Framework

Effective Personal Financial Management requires clear, time-bound objectives. Without goals, a budget is just a list of numbers. You should categorize your financial aspirations into three horizons:

Short-term: Immediate needs or purchases within 12 months.

Medium-term: Major life milestones, such as a Home Loan deposit.

Long-term: Wealth goals for a comfortable retirement and Legacy Preservation.

Writing these goals down and sharing them with family members creates a support network that reinforces your commitment to your Personal Financial Management plan.

3. Advanced Rules for Asset Allocation

Once you have established your goals, you need a system to distribute your capital. Two world-renowned systems used in Personal Financial Management include:

The 50/30/20 Rule: A balanced approach where 50% of income goes to essentials, 30% to personal wants, and 20% is dedicated to Debt Repayment or Savings.

The 6 Jars System: A more granular method that partitions income into specific categories like Education, Giving, and Financial Freedom.

4. Investing: Transitioning from Saving to Wealth Growth

While keeping money in a savings account is low-risk, true Personal Financial Management emphasizes that Investing is the key to significant Capital Appreciation. To make your money work harder, you must explore different Asset Classes that suit your risk profile:

Shares & Real Estate: For long-term growth and potential rental yields.

Time Deposits: Such as the HSBC Step-up Time Deposit, which provides a guaranteed return while offering flexible withdrawal options.

A critical component of any Personal Financial Management plan is the Emergency Fund. Aim to keep at least 3 months of essential expenses in a separate, liquid account to prevent you from having to borrow during a crisis.

5. Mastering Debt and Mitigating Risk

Debt management is a vital pillar of Personal Financial Management. Instead of ignoring liabilities, take stock and prioritize. Utilizing tools like Spend Instalments (0% interest over 12 months) or a Personal Instalment Loan can help consolidate multiple high-interest debts into one manageable, lower-rate payment.

Furthermore, you must protect your Human Capital through insurance. Whether it is Medical Care Insurance or life cover, protecting yourself now ensures that your long-term Personal Financial Management goals aren’t derailed by unforeseen health issues.

6. Conclusion: The Long-Term Vision of Legacy Planning

The final stage of Personal Financial Management is Legacy Planning. In Vietnam, without a lawful will, your estate may be distributed according to heir priority rather than your personal wishes. By integrating inheritance planning into your broader financial strategy early on, you preserve the wealth you have worked a lifetime to build.

Personal Financial Management is an ongoing process of evaluation and adjustment. As your life circumstances change, your budget and goals must evolve. By starting early and maintaining disciplined habits, you ensure that your money doesn’t just sit there—it grows, protects, and provides for generations to come.

Conclusion: Empowering Your Future Through Personal Financial Management

The journey toward financial independence is not a sprint; it is a marathon that requires consistent discipline and a strategic vision. Implementing a robust Personal Financial Management framework is not just about controlling your current cash flow—it is the master key that unlocks doors to high-growth investment opportunities in the future.

By starting with foundational steps—from rigorous budgeting and understanding Asset Allocation to utilizing sophisticated financial leverage—you are laying the solid bedrock for your own “fortress” of prosperity. Remember, the ultimate objective of Personal Financial Management is not merely to accumulate figures on a spreadsheet; it is to create a profound sense of security for yourself and a sustainable Legacy Preservation for the generations to come.

Do not wait for a “perfect” moment to begin. Even the smallest adjustments in your spending habits today can lead to a monumental difference in your Net Worth a decade from now. Master your money, so it never has to master you.